Car insurance isn’t cheap when you’re just starting out, and that’s true whether you’re 17 or 37. For new drivers in the UK, the lack of a driving record, combined with general insurer caution, means one thing: your first premium is likely to be the most expensive you’ll ever pay.

Naturally, many drivers look for the cheapest policy they can find online. But some of those deals come with high excesses, restrictive terms, or limited support when something goes wrong. That’s where technology can offer a smarter solution.

Over the past decade, two tools have quietly reshaped the landscape for first-time drivers: dash cams, black box and app-based telematics car insurance. These aren’t gimmicks, they’re ways to demonstrate your driving habits in real time, proving you’re not the high-risk driver that your quote assumes.

In fact, according to industry data from LexisNexis, drivers using black box policies are 40% less likely to make a claim, and for those who do claim see settlement times reduced thanks to verified journey data.

This article explores how both technologies work, why they help insurers trust you more, and how using them can lead to real, lasting savings. Whether you’re young, mid-career, or simply coming to driving later in life, this guide will help you take control of your costs, not just once, but for the long term.

Why is new driver insurance so expensive in the first place?

New drivers are a question mark. With no claim history and no telematics data to speak of, insurers must assume the worst, and price accordingly. That’s why your first quote often reflects the risks associated with other people like you, rather than anything about your personal driving style.

And while it’s easy to think of expensive insurance as a ‘young person’s problem’, it affects drivers of all ages. If you're 30 and just passed your test, your risk profile is still unproven. Age helps, but experience matters more.

Statistically, new drivers, especially in their first 12 months, are more likely to be involved in accidents than those with several years behind the wheel. Add in unfamiliarity with high-speed roads, night-time driving, or even simple parking manoeuvres, and it’s not hard to see why underwriters proceed with caution.

That doesn’t mean you’re stuck. It means you need to start building trust, and fast. That’s where tools like black boxes and dash cams come in.

How do black boxes (or telematics) help lower your premiums?

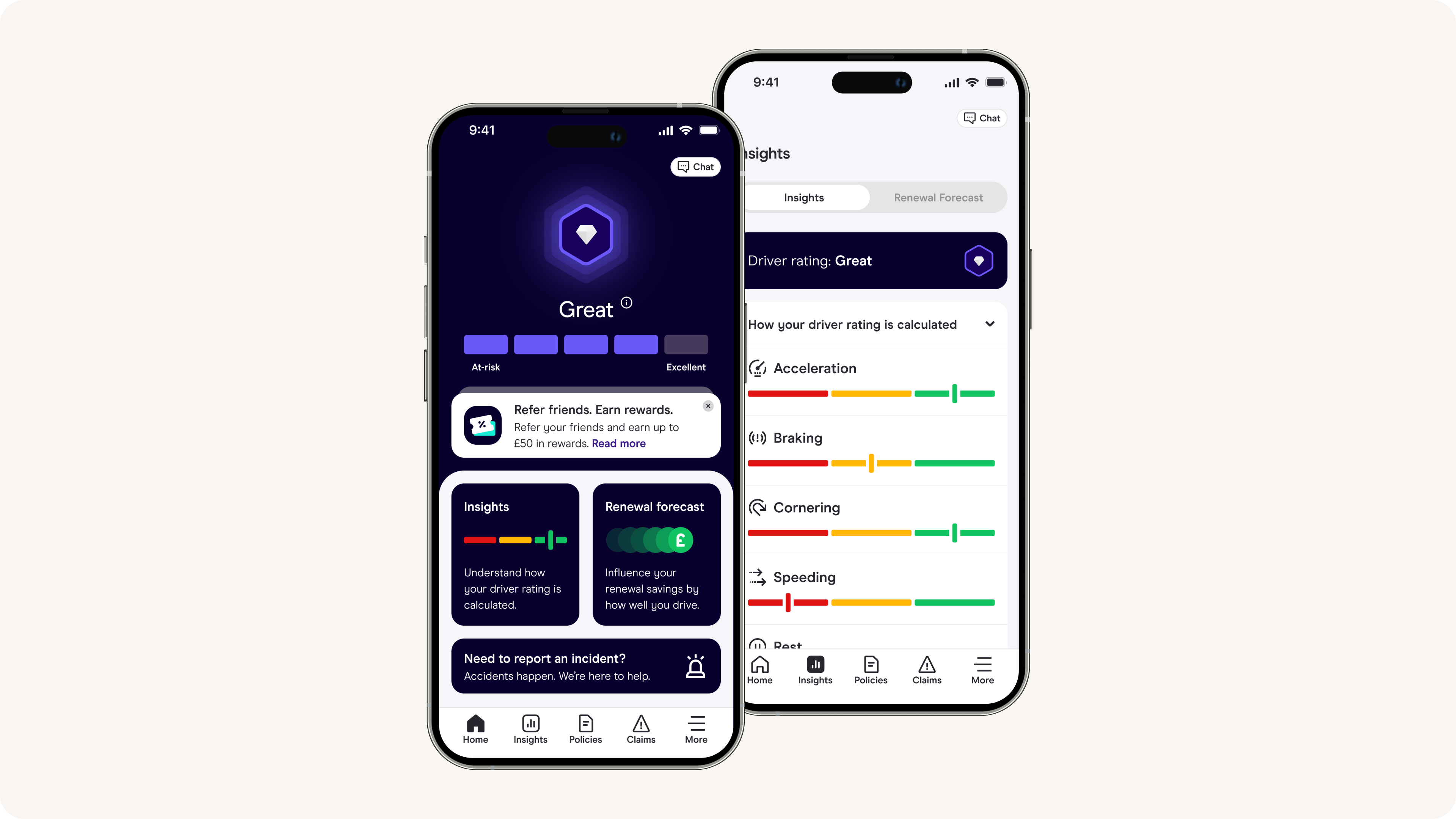

A black box is a small device fitted in your vehicle to monitor how you drive. But technology has moved on. More and more drivers now use app-based telematics insurance like Zego Sense. These apps live on your smartphone and track your driving behaviour, which means there is no need for extra hardware.

They don’t judge you based on your age or postcode. They simply observe how you drive.

Modern telematics tools collect data on:

- How you accelerate and brake

- How you take corners and your average speed

- When you tend to drive

- The types of roads you use – from urban streets to motorways

- Your phone use or distractions behind the wheel (depending on the app)

This data helps build a fairer, more accurate picture of your driving - putting you in control of your insurance, perfect for those looking to build up a driving profile quick, such as learner drivers.

This information is shared with the insurer in real time or at intervals, helping them see you as an individual rather than a statistic. The benefit? If you drive smoothly, avoid harsh braking, and stick to safer times of day, you’re likely to see a reduced premium at renewal.

According to LexisNexis, the average saving from telematics-based insurance for new drivers is around £300–£400 annually, with some policies offering real-time discounts during the policy year.

Unlike old-school black box setups, app-based telematics doesn’t require professional installation and works seamlessly through your phone, making it especially popular among younger drivers who are already used to tracking fitness, mobile banking and consistent screentime.

Want it explained in under 60 seconds?

The TikTok channel Driving Test Success has built a huge following, with over 1.2 million learner drivers, parents, and new drivers, by breaking down driving topics with clarity and confidence.

In one recent post, @drivingtestsuccess on TikTok hits the mark when explaining how black box insurance works.

What do dash cams really do, and how can they save you money?

Dash cams don’t directly track how you drive, but they do offer visual evidence in case of an accident or dispute. For insurers, that means faster claims resolution and clearer liability. For you, it means less hassle and a better chance of defending yourself if you weren’t at fault.

They’re especially helpful in situations involving:

- Disputed blame (e.g., at junctions or roundabouts)

- ‘Crash-for-cash’ fraud

- Vandalism or theft while parked

- Hit-and-run incidents

While having a dash cam won’t automatically reduce your premium, some insurers do offer small discounts, and more importantly, you may be spared a claim being incorrectly recorded as your fault, which could raise future premiums significantly.

High-definition footage also increases your credibility in court or with police investigations. In some cases, footage can even help protect no-claims bonuses or reduce excess charges.

If you’re considering one, the team at What Car? put together a detailed and well-tested roundup of options at different price points. Their guide to the best dash cams covers features like night vision, GPS tagging, and parking protection, all of which can strengthen your case if something goes wrong on the road or off it.

Do all cheap insurance deals include these tools, and what should you avoid?

Not even close. In the search for ‘cheap car insurance for new drivers’, many people are tempted by bare-bones policies that strip out long-term value in favour of short-term savings. These might include:

- High compulsory excess (sometimes £1,000 or more)

- Very low mileage caps

- No provision for telematics or black box discounts

- Poor support during claims

- Expensive add-ons for basics like windscreen repair or legal cover

A truly cost-effective policy should do more than tick the cheapest-price box. It should support safer driving, offer value throughout the year, and adapt to your needs.

Dash cams and telematics aren’t bundled by default, but choosing a policy that rewards your driving behaviour will typically provide far better savings over 12 months than £40 off at the start.

And don’t forget: telematics insurance policies aren’t just for 17-year-olds anymore. Many are open to new drivers aged 25, 35 or even 50, especially those returning to the road or changing countries.

Why using tech and good habits together makes premiums fall over time

Cheap insurance isn't about a one-off deal, it's about proving to insurers that you're not a risk. That takes consistency.

Telematics helps build that trust by showing your driving habits over time. Dash cams help protect your record by giving context when things go wrong. Combined with careful driving, no speeding, limited late-night travel, and keeping distractions low, these tools create a long-term discount cycle.

What you’re doing is reframing yourself from ‘new and unknown’ to ‘safe and proven’. That’s worth far more than a discount code.

And the benefits compound. As you avoid claims, your no-claims discount (NCD) builds. As you clock up years of incident-free driving with good telematics ratings, you become eligible for wider policies at lower prices, including ones that don’t require any monitoring at all.

In other words: the more effort you put in now, the less you’ll pay later.

The smart way to shop for your first car insurance

There’s nothing wrong with wanting cheap car insurance – it’s expensive enough as it is. But not all low-cost policies are built the same. Some might save you money upfront but cost you far more later.

If you’re a new driver, whether you’re 18 or 38, the smarter route is to combine fair pricing with proof. A telematics policy – like Zego Sense – monitors how you accelerate, brake and handle corners, building a personalised picture of your driving. It runs quietly in the background through your phone, helping you earn fairer prices based on how you actually drive.

Add a dash cam to back yourself up in case of a claim. And shop based on total value – not just the opening price.

This kind of control helps you save money now and builds a solid track record for lower premiums down the line.