If you’re a taxi driver, or you use your car for private hire work, you’ll need taxi insurance to keep you covered. It’s a legal requirement for anyone who drives passengers in exchange for money.

As taxi insurance is a specific type of cover for professional drivers, the cost will be different to standard motor insurance. So how much does taxi insurance cost?

On average, private hire taxi drivers with a clean driving record, good claims history and no convictions can expect to pay around £158.28 for a 30-day taxi insurance policy, or around £1,454.34 for an annual policy*.

These prices are based on the average rates paid by Zego customers with a good driving history. The price you’ll pay really depends on your insurer, your driving experience and your driver risk factors.

But before we get into that, let’s cover the basics.

What is taxi insurance?

Taxi insurance for private hire drivers – also known as hire and reward insurance (or H&R for short) – is a type of commercial insurance policy that covers private hire drivers. It’s insurance for people who use their vehicles to carry pre-booked passengers in exchange for payment.

Depending on the level of cover you need, private hire insurance can insure you, your vehicle, your passengers, plus any third-party people and their property.

Private hire taxi insurance is also referred to as PCO insurance or minicab insurance. It specifically covers licensed drivers who carry passengers for a living.

Standard motor insurance (known as social, domestic, and pleasure insurance, or SD&P) won’t cover you for this type of work.

Why does taxi insurance cost more than regular insurance?

Taxi insurance can cost more than regular insurance as taxi drivers cover more miles and drive through congested areas at busier times of day. So the risk of being involved in an accident is higher.

This extra risk drives up the price, which is why taxi insurance is often more expensive than regular car insurance.

What affects the cost of taxi insurance?

It’s good to know which factors can affect the price of your taxi insurance. Here are some of the main ones:

Your driving history

If you’ve been involved in a road traffic accident recently, or since you last got an insurance quote, you might see your price go up.

Even if the accident wasn’t your fault, your insurer will need to consider your claims history when calculating your risk as a taxi driver.

If you have the option to buy no claims discount (NCD) protection with your policy, that can be a good way to keep your costs down in the future. It keeps your discount safe, even if you’re involved in an accident and need to make a claim.

Points on your licence

The same goes for points on your licence. The more you have, the more likely that your insurance cost will rise. Depending on the type of penalty, some points can stay on your licence for years.

If points do get added to your licence, be sure to declare them. Otherwise your insurer might not be able to pay out if you make a claim.

Your vehicle

If your car or minicab is worth a lot of money, you may end up paying a bit more for your insurance. That’s because it would cost your insurer more to repair or replace it if it got damaged.

Expensive vehicles are also more likely to get stolen, as thieves tend to target cars that are worth more. This increased risk can add to the cost of your insurance.

The same goes for powerful vehicles. If your car has a large engine capacity, or has been modified to make it go faster, your insurer might think you’re more likely to be involved in a collision.

Black Cab or Private Hire

For black cab and private hire drivers, insurance needs differ slightly. Black cabs require policies for picking up passengers without pre-booking, while private hire insurance is for pre-arranged bookings only, which can impact the cost and coverage.

If you’re looking for black cab insurance, SimplyQuote offers a comparrsion service with options to meet the specific requirements and risks faced by black cab drivers.

Where you live

Insurers use your postcode and where your vehicle is parked at night to help calculate your risk profile.

If there’s a high crime rate in your area, or your vehicle is parked on a busy street (as opposed to a locked garage), you may end up paying more for your insurance.

So if you move house, always check to see how it will affect the price you pay for your private hire taxi insurance.

Your age

Younger drivers tend to have the least experience on the road, so they usually carry the greatest risk of being involved in an incident. That’s why drivers under 25 tend to pay the most for car insurance.

Drivers in their 50s and 60s are usually considered the safest drivers, especially if they have no previous claims or convictions and a clean driving licence.

Drivers over 70 tend to see a slight increase in their insurance renewals. That’s because, statistically, older drivers are more likely to be involved in a crash and suffer serious injuries.

Criminal convictions

Even if you’re convicted of a non-motor-related crime, there’s a good chance your costs could go up. Criminal convictions add to a more risky driver profile, so your insurer will take that into account when calculating your quote.

It’s worth noting that some insurers will also want to know about spent convictions, so be sure to check what you need to declare.

How to lower the cost of taxi insurance

The cost of your taxi insurance is mostly based on risk. If an insurer thinks the risk of your car getting damaged or stolen is high, you’ll probably pay more than someone they consider to be low risk.

So if you can manage your risk as a driver, you can help to reduce the amount you pay for your taxi insurance.

Here are a few things to get you started:

- Try to keep a clean driving record and your licence free from points.

- Add no claims discount (NCD) protection to your policy, so if you’re involved in an accident you won’t lose your discount.

- Check whether your vehicle is driving up the cost of your insurance.

- If you can, park your vehicle in a secure location overnight and let your insurer know where.

- And check if you’re eligible to switch to Zego Sense – our app-based insurance policy. It could save you a lot of money.

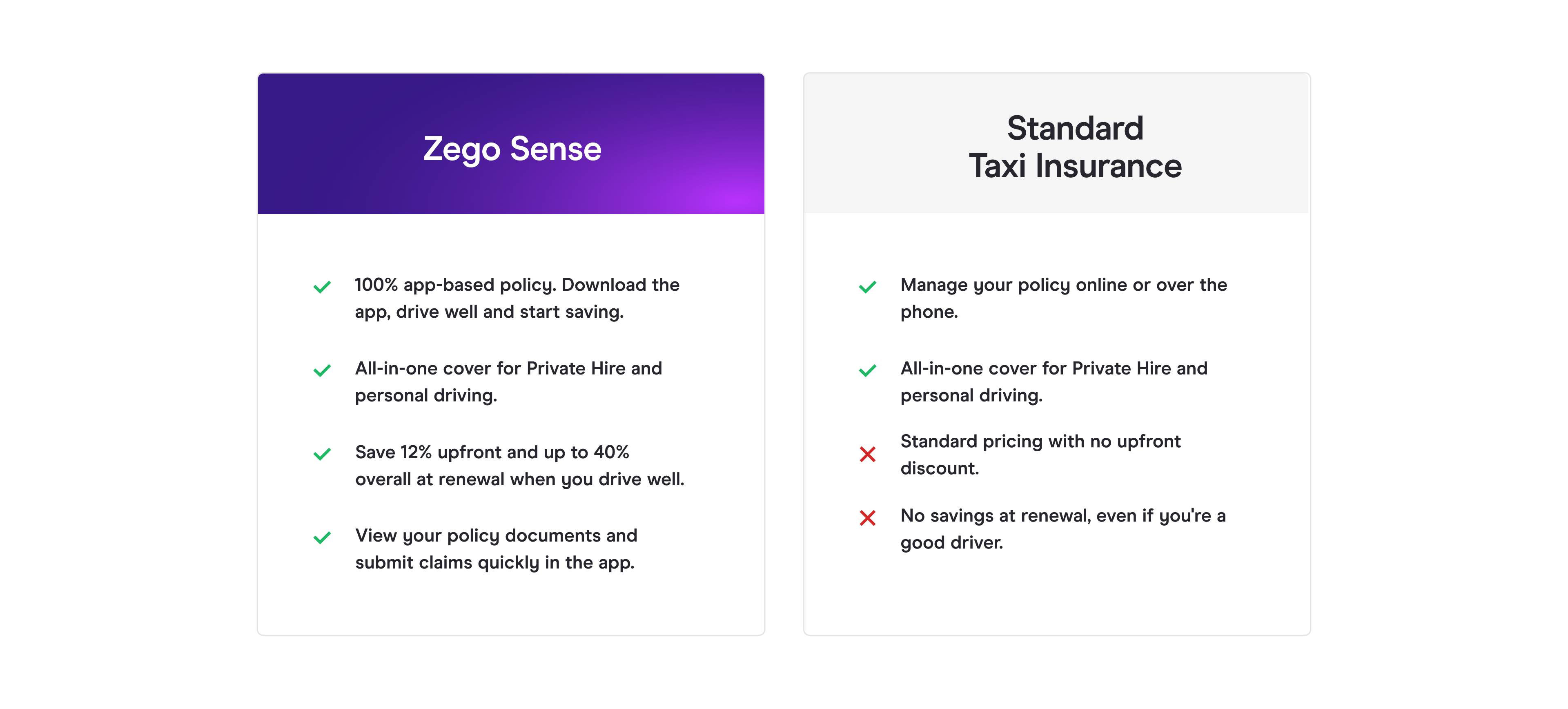

Standard insurance vs Zego Sense

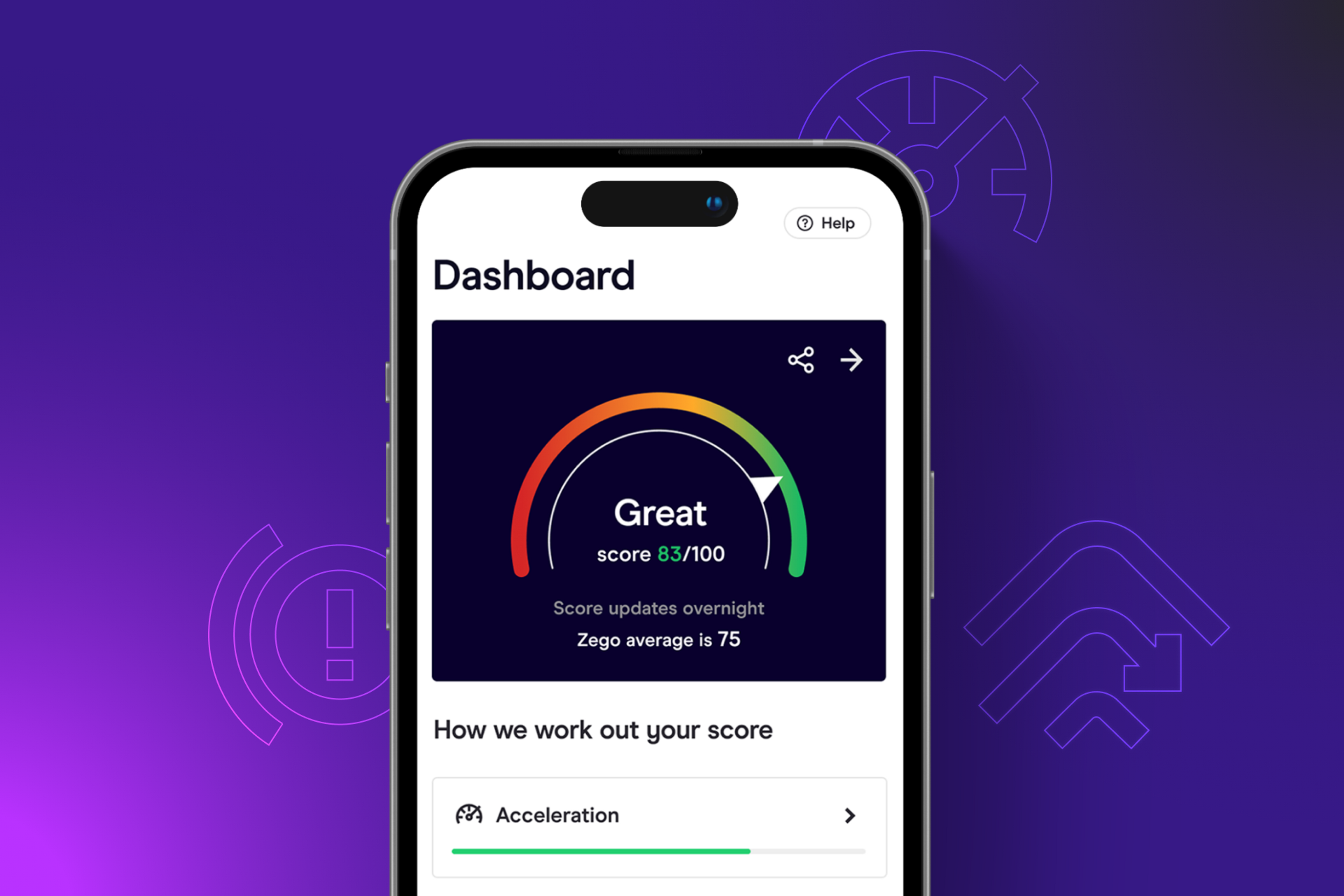

Zego Sense is our clever app-based insurance that rewards good driving with lower prices.

You can save 10%** upfront, just for switching, then get up to 27% off*** overall when you drive safely.

It covers you for private hire and delivery driving (hire & reward), as well as personal use (social, domestic & pleasure).

Here’s how Zego Sense compares with a standard policy:

The Zego Sense app uses your phone’s sensors to measure how you drive. Drive well and you’ll build a high driver score, which means lower insurance costs when you renew.

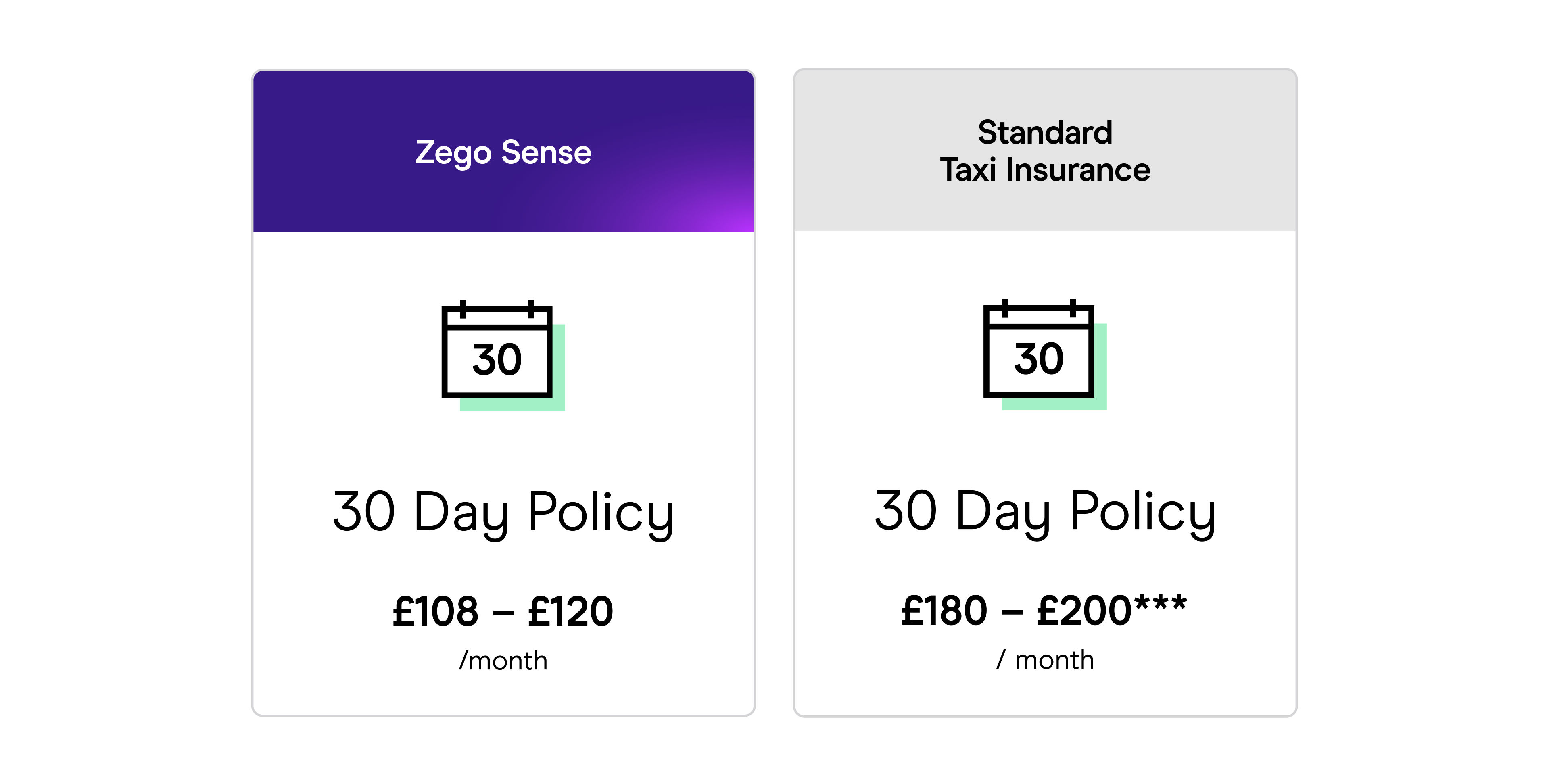

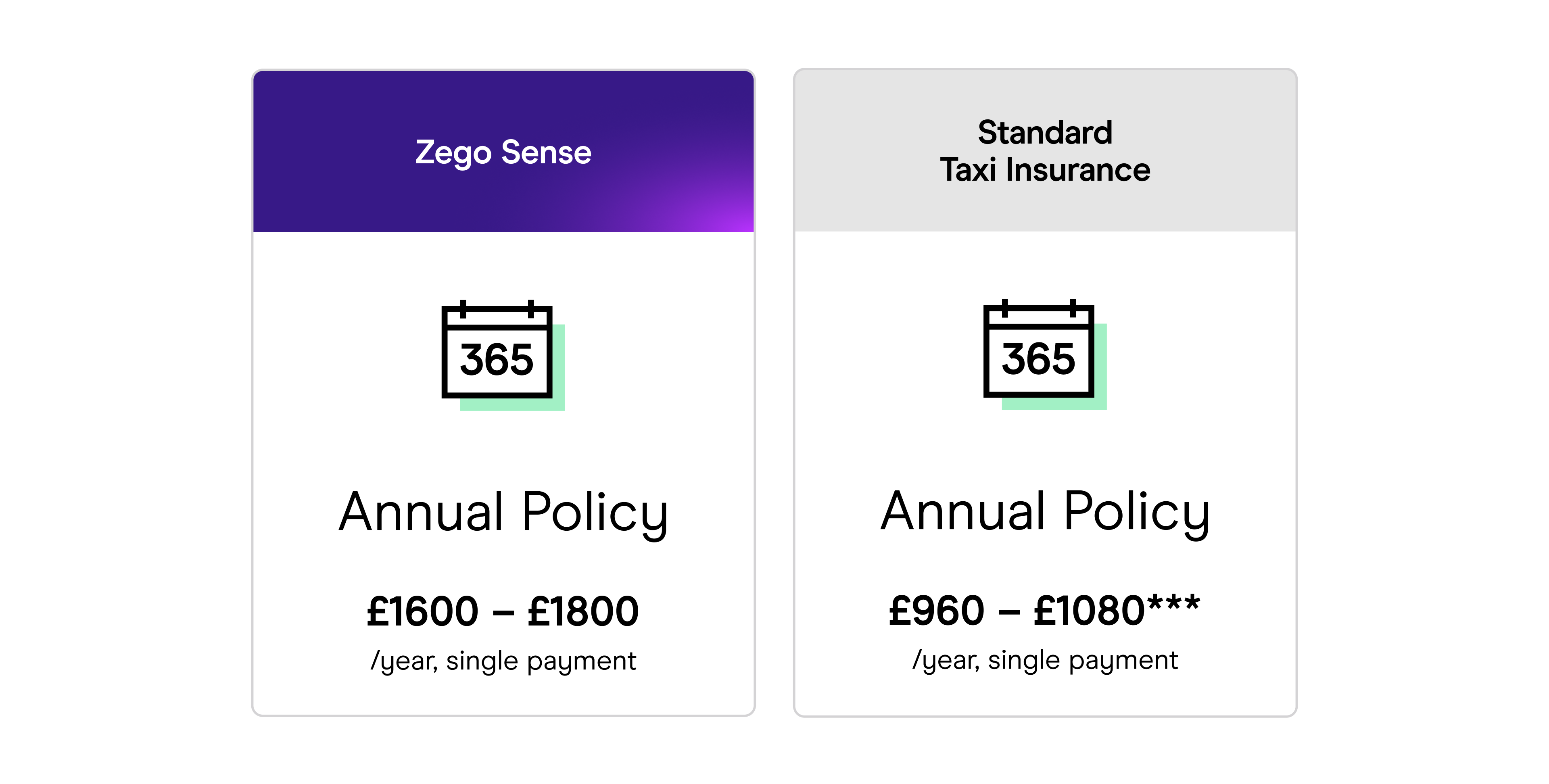

Here’s how much you could save with a Zego Sense policy:

Get a quick quote now — it only takes a minute.

*10% of customers paid this or less in the 6 months prior to 17/10/24

**Based on Zego customers who have been insured on Sense policies and have had a Driver Score, between May 15th 2024 and June 18th 2024